Web3 Lawyers Decode: What kind of RWA do we understand?

Recently, discussions about RWA projects have been fervent in various Web3 communities. Industry observers often assert online that “RWA will reconstruct the new financial ecology of Hong Kong,” believing that relying on the existing regulatory framework of the Hong Kong Special Administrative Region, this track will see breakthrough development. During exchanges and discussions with colleagues, Crypto Salad found that there has been ongoing debate about the so-called “Compliance” issue, with differing understandings of the question “What is compliance?” It often leads to a situation where each side has its own reasoning. This phenomenon arises from the existing differences in understanding of the RWA concept.

Therefore, it is necessary for the encryption salad to discuss the concept of RWA from the perspective of a professional legal team, and to sort out the compliance red lines of RWA.

How should the concept of RWA be defined?

(1) Background and Advantages of RWA Projects

Currently, RWA is becoming the focus of heated discussion in the market and is gradually forming a new wave of development. This phenomenon is mainly based on the following two major backgrounds:

First, because the advantages of the tokens themselves can make up for the shortcomings of traditional financing.

Traditional financial markets have long faced inherent shortcomings such as high entry barriers, long financing cycles, slow financing speeds, and complex exit mechanisms. However, token financing can effectively bypass these defects. Compared with traditional IPOs, RWA has the following significant advantages:

1. Fast financing speed: Due to the circulation of tokens being based on blockchain technology and typically circulating through decentralized intermediary trading institutions, it avoids obstacles such as foreign investment access restrictions, industry policy constraints, and lock-up period requirements that traditional financial projects may encounter. At the same time, it can compress the review process that originally took months or even years, greatly improving the financing speed.

2. Asset Diversification: Traditional IPOs have a single type of asset, only supporting equity issuance, which places strict requirements on the revenue stability, profitability, and asset-liability structure of the issuing entity. However, for RWA, the suitable types of assets are more diverse, encompassing various non-standard assets, which not only expands the range of financeable assets but also shifts the focus of credit assessment to the quality of underlying assets, significantly lowering the qualification threshold for the issuing entity.

3. Relatively low financing costs: Traditional IPOs require long-term collaboration among multiple intermediaries such as investment banks, auditors, and law firms, with the total cost of the listing process potentially exceeding millions or even tens of millions, resulting in substantial expenses. However, RWA issues tokens through decentralized exchanges, saving a significant amount in intermediary fees, while also operating through smart contracts, which eliminates another large portion of labor costs.

In summary, RWA has found itself at the forefront of financing projects due to its unique advantages, while the Web3 world and the cryptocurrency space particularly require funding and projects from the traditional real world. This has led to the current situation where, whether aiming for substantial business transformation or merely wanting to ride the “trend” and gain attention, leading projects in the niche sectors of listed companies, as well as the diverse range of grassroots “quirky” startups, are all actively exploring the application possibilities of RWA.

Second, Hong Kong’s “Compliance” has added fuel to the heat.

Actually, RWA has been developing overseas for a while now. This wave of enthusiasm is due to a series of regulatory innovations passed in Hong Kong, which led to the implementation of several benchmark projects, providing domestic investors with a Compliance channel to participate in “RWA” for the first time. The “Compliance” RWA that Chinese people can access has been realized. This groundbreaking progress not only attracts native encryption assets but also prompts traditional projects and funds to start paying attention to the investment value of RWA, ultimately driving the market enthusiasm to new heights.

However, do users who want to try RWA really understand what RWA is? There are various RWA projects, with different underlying assets and operational structures. Can everyone distinguish their differences? Therefore, we believe it is necessary to clearly define what constitutes compliant RWA through this article.

People generally believe that RWA is a financing project that tokenizes underlying real-world assets through blockchain technology. However, when we delve into the underlying assets of each project and trace back the operation process of the project, we find that the underlying logic of these projects is actually different. We have conducted a systematic study on this issue and summarized the following understanding of the concept of RWA:

We believe that RWA is actually a broad concept and there is no so-called “standard answer”. The process of asset tokenization through blockchain technology can all be referred to as RWA.

(2) Elements and Characteristics of RWA Projects

Real RWA projects need to have the following characteristics:

1. Based on real assets

The authenticity of the underlying assets and whether the project can establish a transparent and acceptable off-chain asset verification mechanism with third-party audits are key criteria for determining whether the project’s tokens will achieve effective value recognition in reality. For example, PAXG issues tokens that are anchored to gold in real-time, with each token backed by 1 ounce of physical gold. The gold reserves are managed by a third-party platform and are subject to quarterly audits by a third-party auditing company, even allowing for the redemption of a corresponding amount of physical gold using the tokens. This highly transparent and regulated asset verification mechanism enables the project to gain investor trust and provides a foundation for effective valuation within the real financial system.

2. Asset Tokenization on Chain

Asset tokenization refers to the process of converting real-world assets into digital tokens that can be issued, traded, and managed on the blockchain through smart contracts and blockchain technology. The value flow and asset management processes of RWA are automated through the execution of smart contracts. Unlike traditional financial systems that rely on intermediaries for transactions and settlements, RWA projects leverage smart contracts to achieve transparent, efficient, and programmable business logic execution on the blockchain, thus significantly enhancing asset management efficiency and reducing operational risks.

Asset tokenization endows RWA with key characteristics of being divisible, tradable, and highly liquid. After asset tokenization, assets can be divided into small tokens, lowering the investment threshold, changing the way assets are held and circulated, and allowing retail investors to participate in markets that were originally high-threshold.

3. Digital assets have ownership value

The tokens issued by RWA projects should belong to digital assets with property attributes. The project parties should clearly distinguish between data assets and digital assets: data assets are collections of data owned by enterprises that can create value. In contrast, digital assets are the value itself and do not require repricing through data. To illustrate, when you design a painting, upload it to the blockchain, and generate an NFT, this NFT is a digital asset because it can be authenticated and traded. However, the large amount of feedback from users about this painting, browsing data, click-through rates, and other data you collected belong to data assets. You can analyze data assets to understand user preferences, improve your work, and adjust its price.

4. The issuance and circulation of RWA tokens comply with legal regulations and are subject to administrative supervision

The issuance and circulation of RWA tokens must operate within the existing legal framework; otherwise, it may not only lead to project failure but also trigger legal risks. First, real-world assets must be genuine, legal, and have clear ownership without disputes, so they can serve as the basis for token issuance. Secondly, RWA tokens usually possess rights to revenue or asset interests, making them easily recognized as securities by regulatory agencies in various countries; therefore, compliance with local securities regulations must be carried out before issuance. The issuing entity must also be a qualified institution, such as one holding asset management or trust licenses, and must complete KYC and anti-money laundering procedures. Once entering the circulation phase, the trading platforms for RWA tokens also need to be regulated, typically requiring compliance with exchanges or secondary markets with financial licenses, and trading on decentralized platforms is not allowed. Furthermore, continuous information disclosure is necessary to ensure that investors can obtain real information regarding the assets linked to the tokens. Only within such a regulatory framework can RWA tokens be issued and circulated legally and safely.

In addition, the compliance management of RWA has typical cross-jurisdictional characteristics. Therefore, it is necessary to construct a systematic compliance framework that covers the legal norms of the asset location, the flow of funds, and various regulatory authorities. Throughout the entire lifecycle of asset on-chain, cross-chain, and token cross-border and cross-platform circulation, RWA must establish a compliance mechanism that includes multiple aspects such as asset confirmation, token issuance, fund flow, profit distribution, user identification, and compliance audit. This not only involves legal consulting and compliance design but may also require the introduction of third-party trust, custody, auditing, and regulatory technology solutions.

(3) Types and Regulations of RWA Projects

We found that there are two parallel types among the RWA projects that meet the requirements:

1. Narrow Definition of RWA: Physical Assets on the Blockchain

We believe that the narrow definition of RWA specifically refers to projects that tokenize real assets with authenticity and verifiability on the blockchain, which is also the common understanding of RWA among the public. Its application market is the most extensive, such as projects that anchor tokens to offline real assets like real estate, gold, etc.

2. STO (Security Token Offering): Financial Assets on the Blockchain

Except for the narrow definition of RWA projects, we have found that a large number of RWA projects currently in the market are STOs.

(1) Definition of STO

According to the differences in underlying assets, operating logic, and token functions, the existing tokens in the market can generally be divided into two categories: Utility Tokens and Security Tokens. STO refers to the process of financializing real assets and issuing tokenized shares or certificates on the blockchain in the form of Security Tokens.

(2) Definition of Security Tokens

Security tokens, in contrast to utility tokens, are simply financial products on the blockchain that are governed by securities regulations, similar to electronic stocks.

(3) Regulation of Security Tokens

Under the regulatory framework of mainstream encryption asset-friendly countries such as the United States and Singapore, once a token is identified as a security token, it will be bound by traditional financial regulatory agencies (such as the Securities and Exchange Commission), and the token design, trading models, etc. must comply with local securities regulations.

From an economic perspective, the core objective of financial products is to coordinate the supply and demand relationship between financing parties and investors; from a legal and regulatory standpoint, some countries focus more on protecting investor interests, while others are more inclined to encourage the smoothness and innovation of financing activities. This difference in regulatory stance is reflected in the specific rules, compliance requirements, and enforcement strength within the legal systems of various countries. Therefore, when designing and issuing RWA products, it is essential to consider not only the authenticity and legality of the underlying assets but also to conduct a comprehensive review and compliance design of key aspects such as product structure, issuance methods, circulation paths, trading platforms, investor access thresholds, and capital costs.

It is especially worth noting that once the core attraction of a certain RWA project comes from its high leverage and high return expectations, and positions “hundredfold, thousandfold returns” as the main selling point, then regardless of its superficial packaging, its essence is very likely to be classified as a securities product by regulators. Once identified as a security, the project will face a more stringent and complex regulatory system, greatly increasing its subsequent development path, operating costs, and even legal risks.

Therefore, when discussing the legal compliance of RWA, we need to deeply understand the connotation of “securities regulations” and the regulatory logic behind it. Different countries and regions have different definitions and regulatory focuses on securities. The United States, Singapore, and Hong Kong have all defined the criteria for classifying security tokens. It is not difficult to find that the classification method is essentially to determine whether the tokens meet the local securities regulations’ criteria for “securities”; once the securities conditions are satisfied, they fall into the category of security tokens. Therefore, we have organized the relevant provisions from key countries (regions) as follows:

A. Mainland China

In the regulatory framework of mainland China, the “Securities Law of the People’s Republic of China” defines securities as stocks, corporate bonds, depository receipts, and other negotiable securities recognized by the State Council, and also includes the listing and trading of government bonds and shares of securities investment funds within the regulation of the “Securities Law.”

(The above image is taken from the Securities Law of the People’s Republic of China)

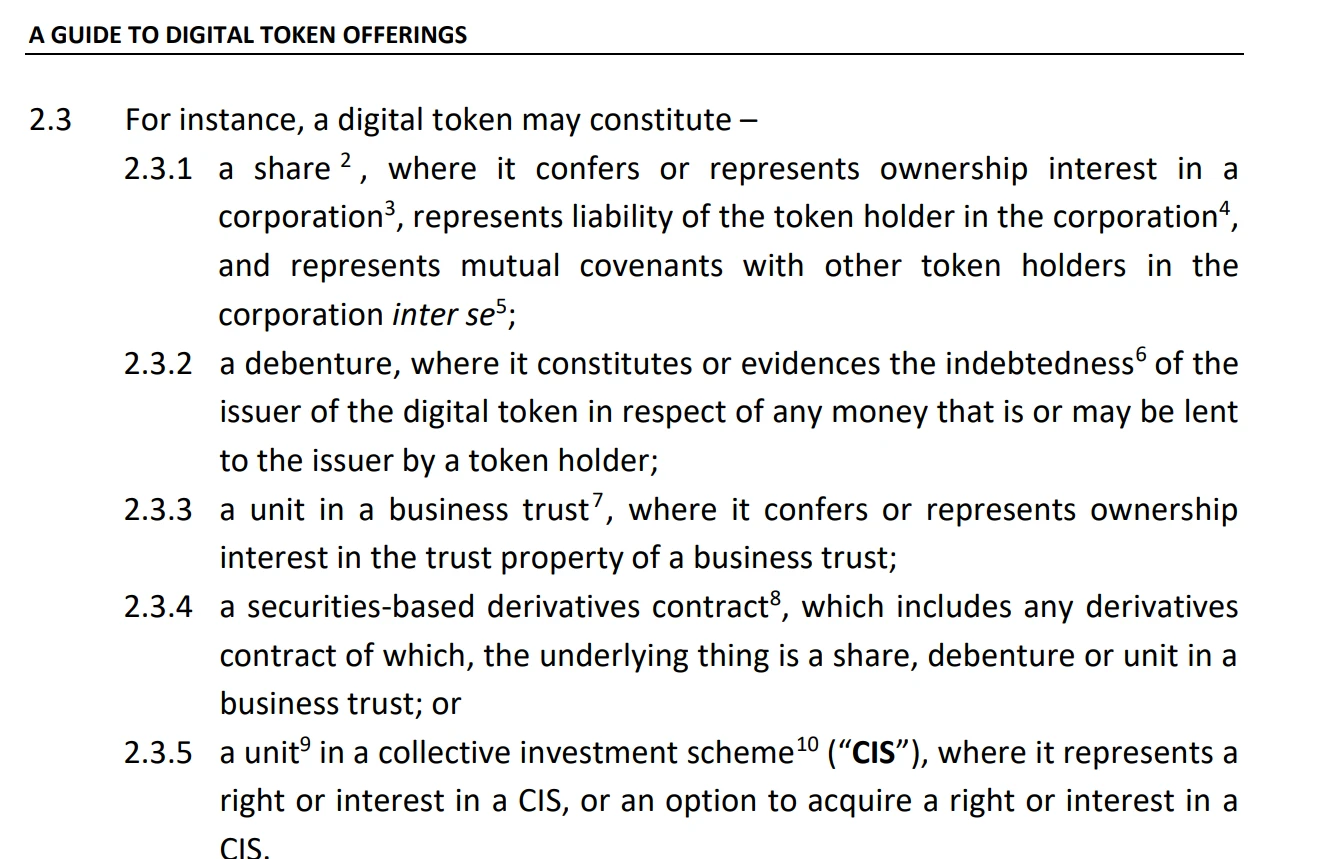

B. Singapore

Although Singapore’s “Digital Token Offering Guidelines” and “Securities and Futures Act” do not directly mention the concept of “security tokens,” they detail the different circumstances under which tokens may be classified as “capital market products:”

(The above image is taken from the “Digital Token Issuance Guide” )

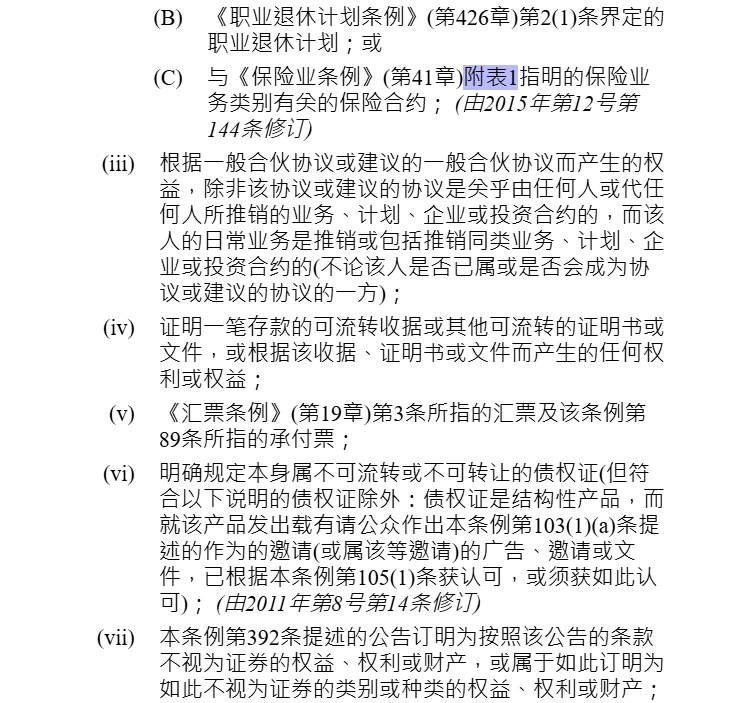

C. Hong Kong, China

The Securities and Futures Commission in the Hong Kong region of China has specific enumerative provisions regarding the positive and negative lists of securities in the Securities and Futures Ordinance.

(The above image is excerpted from the Securities and Futures Ordinance )

The regulation defines “securities” as including “shares, equity shares, notes, bonds” structured products, and does not limit their existence to traditional carriers. The SFC has clearly pointed out in the “Circular on Intermediaries Engaging in Activities Related to Tokenized Securities” that the nature of its regulatory targets is essentially traditional securities packaged as tokenized.

D. United States

The U.S. Securities and Exchange Commission (SEC) stipulates that any product that passes the Howey Test will be classified as a security. Any product classified as a security is subject to SEC regulation. The Howey Test is a legal standard established by the U.S. Supreme Court in the 1946 case of SEC v. W.J. Howey Co., used to determine whether a transaction or scheme constitutes an “investment contract” and thus falls under the jurisdiction of U.S. securities law.

The Howey Test lists four conditions under which a financial product is considered a “security.” The application of the Howey Test in digital assets is outlined in the U.S. SEC’s “Framework for ‘Investment Contract’ Analysis of Digital Assets.” We will conduct a detailed analysis on this next:

- The Investment of Money

Refers to investors investing money or assets into a project in exchange for certain rights or expected returns. In the digital asset field, whether purchasing tokens with fiat currency or encryption currency, as long as there is a value exchange behavior, it can generally be recognized as meeting this standard. Therefore, most token issuances basically comply with this condition.

- 共同事业(Common Enterprise)

“Joint ventures” refer to the close binding of interests between investors and issuers, usually manifested as the returns of investors being directly related to the operational effectiveness of the project. In token projects, if the returns of token holders depend on the business development of the project party or the operational results of the platform, it meets the characteristics of a “joint venture,” and this condition is also relatively easy to establish in reality.

- Reasonable Expectation of Profits Derived from Efforts of Others

This point is key in determining whether a token will be classified as a security token. This condition refers to the situation where, if investors purchase a product with the expectation of future appreciation or other economic returns, and such returns are not derived from their own use or operational activities, but rather depend on the overall development of a project created by the efforts of others, then that product may potentially be viewed as a “security.”

In the context of RWA projects, if the purpose of an investor purchasing tokens is to obtain future appreciation or economic returns, rather than benefits derived from personal use or operational activities, then the token may have “profit expectation,” thereby triggering the determination of securities attributes. Particularly, when the returns of the token highly depend on the professional operations of the issuer or project team, such as liquidity design, ecosystem expansion, community building, or cooperation with other platforms, this characteristic of “relying on the efforts of others” further strengthens its potential for securitization.

Tokens with sustainable value in the true sense should be directly anchored to the real returns generated by underlying real-world assets, rather than relying on market speculation, narrative packaging, or platform premiums to drive their value growth. If the value fluctuations of the tokens primarily stem from the “recreation” by the team behind or the platform operations, rather than the returns of the assets themselves, then it does not possess the characteristics of “narrow RWA,” and is more likely to be viewed as a security token.

The U.S. SEC has introduced the Howey Test in its regulation of encryption tokens, which means it no longer relies on the form of the tokens to determine its regulatory stance, but instead shifts to a substantive review: focusing on the actual functionality of the tokens, the method of issuance, and investor expectations. This change marks a trend towards stricter and more mature legal positioning of U.S. regulatory agencies regarding crypto assets.

What is the legal logic behind the “Compliance” tier of the RWA project?

After discussing so much about the concepts and definitions of RWA, let’s return to the core question raised at the beginning of the article, which is also a focal point of widespread concern in the industry:

As RWA has developed to this day, which types of RWA can be considered truly “compliant” RWA? How can we meet the compliance of RWA projects in practice?

First of all, we believe that Compliance means being regulated by local regulatory authorities and adhering to the provisions of the regulatory framework. In our understanding, the compliance of RWA is a layered system.

Layer One: Sandbox Compliance

This specifically refers to the Ensemble sandbox project designed by the Hong Kong Monetary Authority (HKMA), which is currently the narrowest and most regulatory pilot definition of “Compliance”. The Ensemble sandbox encourages financial institutions and technology companies to explore technological and model innovations of tokenization applications through projects like RWA in a controlled environment, to support its leading digital Hong Kong dollar project.

The Hong Kong Monetary Authority (HKMA) has shown a high level of emphasis on the sovereignty of future currency systems in promoting the Central Bank Digital Hong Kong Dollar (e-HKD) and exploring regulations for stablecoins. The competition between central bank digital currencies and stablecoins is essentially a redefinition and contestation of “monetary sovereignty.” The sandbox provides project teams with a certain degree of policy space and flexibility, which is conducive to promoting exploratory practices of bringing real assets onto the blockchain.

At the same time, the Monetary Authority is actively guiding the development of tokenized assets, attempting to expand their applications in real scenarios such as payments, settlements, and financing within a Compliance framework. Several technology and financial institutions, including Ant Group, are members of the sandbox community, participating in the construction of the digital asset ecosystem. Projects entering the regulatory sandbox mean, to some extent, a higher level of compliance and policy recognition.

However, from the current situation, such projects are still in a closed operating state and have not yet entered the broad secondary market circulation stage, indicating that there are still real challenges in asset liquidity and market connectivity. Without a stable funding supply mechanism and efficient secondary market support, the entire RWA token system is difficult to form a true economic closed loop.

Layer Two: Hong Kong Administrative Regulatory Compliance

As an international financial center, Hong Kong Special Administrative Region has been continuously advancing institutional exploration in the virtual asset field in recent years. As the first region in China to clearly promote virtual assets, especially the development of tokenized securities, Hong Kong has become a target market for many mainland project parties eager to try their luck, thanks to its open, Compliance, and clearly defined regulatory environment.

By combing through the relevant circulars and policy practices issued by the Hong Kong Securities and Futures Commission, it is not difficult to find that the core of Hong Kong’s supervision of RWA is actually to incorporate it into the framework of STO and then manage it in compliance. In addition, the SFC has established a relatively complete virtual asset service provider (VASP) and virtual asset trading platform (VATP) licensing system, and is preparing to issue a second virtual asset policy statement to further clarify the regulatory attitude and basic principles when combining virtual assets with real assets. Under this institutional framework, tokenized projects involving real-world assets, especially RWA, have been brought under a higher level of compliance supervision.

From the perspective of existing RWA projects in Hong Kong that have already been implemented and have a certain market influence, most projects possess clear securities attributes. This means that the tokens they issue involve ownership, income rights, or other transferable rights of real assets, which can constitute “securities” as defined under the Securities and Futures Ordinance. Therefore, these types of projects must be issued and circulated through Security Token Offerings (STO) in order to obtain regulatory approval and achieve compliance in market participation.

In summary, Hong Kong’s regulatory positioning on RWA has become quite clear: any mapping of real assets with securities attributes on the blockchain should be included in the STO regulatory framework. Therefore, we believe that the current development path of RWA promoted by Hong Kong is essentially a specific application and practice of the tokenization of securities (STO) path.

Third Layer: Clear Regulatory Framework for Encryption-Friendly Areas

In regions with an open attitude towards virtual assets and relatively mature regulatory mechanisms, such as the United States, Singapore, and certain European countries, a more systematic compliance path for the issuance, trading, and custody of encryption assets and their mapped real-world assets has been established. RWA projects in such regions can be considered compliant RWAs operating under a clear regulatory framework if they can legally obtain the corresponding licenses and comply with information disclosure and asset compliance requirements.

Fourth Layer: “General Compliance”

This refers to compliance in the broadest sense, as opposed to “non-compliance”. It specifically refers to RWA projects within certain offshore jurisdictions where the government temporarily adopts a “laissez-faire” approach towards the virtual asset market, and it has not been explicitly deemed non-compliant or illegal. Its business model has certain compliance space within the local legal framework. Although the scope and concept of this compliance are somewhat vague and do not yet constitute complete legal confirmation, it falls under the business status of “what is not prohibited by law is allowed” before legal regulation becomes clear.

In reality, we can observe that the vast majority of RWA projects find it difficult to achieve the first two types of Compliance. Most projects choose to attempt the first three paths—namely relying on the lenient policies of certain encryption “friendly” judicial jurisdictions to try to bypass sovereign regulatory boundaries and achieve formal “Compliance” at a lower cost.

As a result, the RWA projects are seemingly “sprouting like dumplings” continuously, but the real moment for generating substantial financial value has yet to arrive. A fundamental turning point will depend on whether Hong Kong can clearly explore the secondary market mechanism for RWA—especially how to open up the channels for cross-border capital circulation. If RWA trading remains confined to a closed market aimed at local retail investors in Hong Kong, both asset liquidity and the scale of funds will be extremely limited. To achieve a breakthrough, it is essential to allow global investors to invest in Chinese-related assets through compliance mechanisms, indirectly “buying the dip in China” in the form of RWA.

The role that Hong Kong plays here can be likened to the significance of Nasdaq for global tech stocks in the past. Once the regulatory framework matures and the market structure becomes clear, when Chinese people want to “go abroad” to seek financing, and foreigners want to “buy the dip” on Chinese assets, the first stop will definitely be Hong Kong. This will not only be a regional policy dividend but also a new starting point for the reconstruction of financial infrastructure and capital market logic.

In summary, we believe that the compliance of RWA projects should be conducted within the current framework, and all projects must maintain policy sensitivity. Once there are legal adjustments, urgent changes must be made. In the context where current regulations have not yet been fully clarified and the RWA ecosystem is still in the exploration stage, we strongly recommend that all project parties take the initiative to carry out “self-compliance” work. Although this means investing more resources and incurring higher time and compliance costs at the initial stage of the project, in the long run, it will significantly reduce systemic risks in legal, operational, and even investor relations aspects.

Among all potential risks, the fundraising risk is undoubtedly the most deadly hidden danger for RWA. Once a project design is deemed illegal fundraising, it will face significant legal consequences regardless of whether the assets are real or the technology is advanced, posing a direct threat to the survival of the project itself and delivering a heavy blow to the assets and reputation of the enterprise. During the development of RWA, there will inevitably be differences in compliance definitions across different regions and regulatory environments. For developers and institutions, it is essential to formulate detailed phased compliance strategies based on their own business types, asset attributes, and the regulatory policies of the target market. Only under the premise of ensuring controllable risks can the implementation of RWA projects be steadily advanced.

Lawyer’s Advice on RWA Projects

In summary, as a legal team, we systematically outline the core aspects that need attention from a compliance perspective in the full-chain advancement of RWA projects.

1. Choose a policy-friendly jurisdiction

In the current global regulatory landscape, the compliance advancement of RWA projects should prioritize jurisdictions with clear policies, mature regulatory systems, and an open attitude towards virtual assets, which can effectively reduce the uncertainty of compliance.

2. The underlying assets must have real redeemable capability

No matter how complex the technical architecture is, the essence of RWA projects is still to map the rights of real-world assets onto the chain. Therefore, the authenticity of the underlying assets, the reasonableness of the valuation, and the executability of the redemption mechanism are all core factors that determine the credibility of the project and its market acceptance.

3. Obtain investor recognition

The core of RWA lies in asset mapping and rights confirmation. Therefore, whether the final buyer or user of the off-chain asset recognizes the rights represented by the on-chain token is key to the project’s success or failure. This is not only related to the individual willingness of investors, but also closely related to the legal attributes of the token and the clarity of rights.

While RWA project parties are promoting the compliance process, they must also face another core issue: investors must be informed. In reality, many projects package risks with complex structures and do not clearly disclose the underlying asset status or token model logic to the outside, leading investors to participate without a full understanding. Once fluctuations or risk events occur, it not only triggers a crisis of market trust but may also attract regulatory attention, making the situation often more difficult to handle.

Therefore, establishing a clear mechanism for investor screening and education is crucial. RWA projects should not be open to all groups but should consciously introduce mature investors with a certain risk tolerance and financial understanding. In the early stages of the project, it is especially necessary to set certain thresholds, such as a professional investor certification mechanism, participation limits, and risk disclosure presentations, to ensure that entrants are “informed and voluntary” and truly understand the asset logic behind the project, Compliance boundaries, and market liquidity risks.

4. Ensure that the institutional operators in the link comply with regulations

In the entire process of RWA, it often involves multiple links such as fundraising, custody, valuation, tax processing, and cross-border Compliance. Each link corresponds to regulatory agencies and Compliance requirements in reality, and project parties must complete Compliance declarations and regulatory connections within the relevant legal framework to reduce legal risks. For example, in the part involving fund raising, special attention should be paid to whether it triggers Compliance obligations related to securities issuance, anti-money laundering, and so on.

5. Prevent post-event Compliance risks

Compliance is not a one-time action. After the implementation of the RWA project, it must continue to face changes in the dynamic regulatory environment. How to prevent potential administrative investigations or compliance accountability in the post-event dimension is an important guarantee for the sustainable development of the project. It is recommended that the project party establish a professional compliance team and maintain a communication mechanism with regulatory agencies.

6. Brand Reputation Management

In the highly sensitive virtual asset industry regarding information dissemination, RWA projects also need to focus on public opinion management and market communication strategies. Building a transparent, trustworthy, and professional project image helps to enhance public and regulatory trust, creating a favorable external environment for long-term development.

Conclusion

In the current process of continuous integration between virtual assets and the real economy, various RWA projects have different intentions and mechanisms, featuring both technological innovations and financial experiments. The capabilities, expertise, and practical paths of different projects vary greatly, warranting our detailed study and classification.

Through extensive research and project participation, we have also deeply realized that for market participants, the biggest challenge often lies not in the technical aspects, but in the uncertainty of the system, especially the unstable factors in administrative and judicial practices. Therefore, what we need more is to explore the “practical standards”—even if we do not have legislative and regulatory power, promoting the standardization and compliance of the industry in practice still holds value. As long as there are more participants, the paths mature, and regulatory agencies develop sufficient management experience, the system will gradually improve. Within a legal framework, promoting cognitive consensus through practice and driving institutional evolution through consensus represents a “bottom-up” positive institutional evolution for society.

But we must also maintain the Compliance alarm. Respecting the existing judicial and regulatory framework is the basic premise of all innovative activities. Regardless of how the industry develops or how technology evolves, the law remains the bottom-line logic that safeguards market order and public interests.

This represents the personal views of the author of this article and does not constitute legal advice or opinions on specific matters.