O crescente foco do DeFi na acumulação de valor do Token

Os protocolos DeFi estão sob crescente pressão para recompensar os detentores de tokens com uma parte de suas receitas, e grandes players como Aave, Ethena e Hyperliquid já estão explorando formas de pilotar mecanismos de acúmulo de valor para seus tokens nativos.Se gastou 8-9 figuras em crescimento e não vê a escala de receitas pelo menos linearmente, a recompra não é uma coisa má.

Um dos principais motivos por trás dessa mudança? A vitória na eleição de Donald Trump que trouxe um ambiente regulatório mais favorável para DeFi

Aqui está uma análise das últimas atualizações de tokenomics para Aave, Athena, Jupiter e Hyperliquid, incluindo os seus planos de recompra e alterações de taxa de comutação.

AAVE

Aave acabou de lançar uma grande reformulação de tokenomics, focando em recompras, distribuição de taxas e melhores incentivos para detentores de tokens. Segundo Marc Zeller, fundador da Iniciativa Aave Chan (ACI), esta é uma das maiores propostas na história da Aave.

Buybacks & Fee Switch

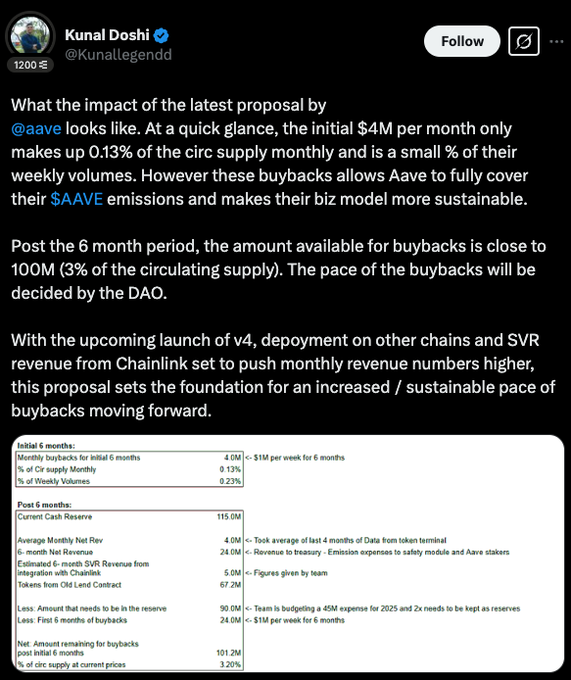

- Aave lançou um programa de recompra de seis meses, reservando $1M por semana (~$4M mensais) para ajudar a cobrir as emissões de AAVE e tornar o protocolo mais sustentável.

- Após seis meses, o pool de recompra poderá atingir $100M (~3% do fornecimento em circulação), cabendo à DAO decidir com que rapidez o implementar.

O objetivo? Manter as emissões sob controlo enquanto fortalece o tesouro da Aave.

Novas Movimentações de Tesouraria e Governança

- Aave está a criar o Comité de Finanças da Aave (CFA) para lidar com os fundos do tesouro e estratégias de liquidez.

- O plano também finaliza a transição longe do LEND, recuperando 320.000 AAVE (~$65M) para uso futuro potencial.

Guarda-chuva: Novo Sistema de Gestão de Risco da Aave

- A Aave gasta $27M por ano em custos de liquidez, por isso estão a introduzir o Umbrella, um sistema para otimizar a eficiência de capital e reduzir os riscos.

- Será integrado em várias blockchains, incluindo Ethereum, Avalanche, Arbitrum, Gnosis e Base.

Anti-GHO: Novas recompensas para detentores de stablecoins

- O Anti-GHO, um novo mecanismo de recompensa, irá substituir o antigo modelo de desconto para os detentores de GHO.

- Os tokens podem ser queimados 1:1 contra dívida GHO ou convertidos em StkGHO, ligando diretamente incentivos à receita da Aave.

- Ainda está em desenvolvimento e pode fazer parte de uma futura atualização "Aavenomics Parte Dois".

O que se segue?

Com o Aave v4, mais implantações de cadeias e fluxos de receita adicionais do SVR da Chainlink, esta atualização lança as bases para recompras maiores e mais sustentáveis no futuro.

Júpiter

Jupiter começou a usar 50% das suas taxas de protocolo para comprar e bloquear tokens JUP por três anos a partir de 17 de fevereiro de 2025.

- Esta iniciativa tem como objetivo reduzir o fornecimento em circulação, aumentar a estabilidade a longo prazo e impulsionar a participação no ecossistema Solana.

- Em fevereiro, Júpiter executou sua primeira recompra, adquirindo 4.88 $JUPpor $3.33M.

- Atualmente, o programa de recompra de truste da Caixa de Areia de Júpiter ultrapassou os 10M $JUP(~$6M).

O que se segue?

Anualizado, o número de $3.33M significa mais de $35M em volume anual de recompra. Tomando um número mais agressivo, Júpiterreceita para 2024 é $102M, significando que se traduzirá em volume de recompra superior a $50M.

Hyperliquid

Hyperliquid’s $HYPEtem um fornecimento de tokens de 1B e sem captação de recursos, o que significa nenhuma alocação de investidores. A distribuição é a seguinte:

- 31.0%: Distribuído por via aérea aos utilizadores iniciais (totalmente líquido).

- 38.888%: Reservado para futuras emissões e recompensas da comunidade.

- 23.8%: Alocação da equipe, bloqueada por 1 ano, com a maioria das ações restritas entre 2027-2028.

- 6.0%: Fundação Hyper.

- 0.3%: Bolsas comunitárias.

- 0.012%: HIP-2.

A relação equipa-comunidade é de 3:7, e o maior detentor não pertencente à equipa é o Fundo de Assistência (FA), detendo 1.16% do fornecimento total e 3.74% do fornecimento em circulação.

Modelo de Receitas & Recompras

A receita da Hyperliquid provém principalmente de taxas de negociação (spot e derivados) e taxas de leilão do HIP-1. Uma vez que a Hyperliquid L1 ainda não cobra taxas de gás, a receita relacionada com gás é excluída.

Alocação de Receitas:

- 46% das taxas de negociação perpétua vão para os detentores de HLP (recompensas do lado da oferta).

- 54% é usado para recompras de HYPE através do Fundo de Assistência (AF).

As fontes de receita adicionais incluem as taxas de leilão do HIP-1 e as taxas de negociação à vista (parte em USDC), atualmente alocadas para recompras da HYPE.

Em resumo, o Hyperliquid implementa uma estratégia deflacionária dupla para HYPE:

- Buyback — o Fundo de Assistência (AF) usa uma parte das receitas para recomprar tokens HYPE do mercado, os tokens são mantidos pelo AF em vez de serem queimados

- Queimar — todas as taxas de negociação à vista pagas em HYPE (como pares HYPE-USDC) são queimadas + todas as taxas de gás na HyperEVM (uma vez totalmente ativa na mainnet) serão pagas em HYPE e queimadas

Impacto da recompra & Stake

- Existem muitas fontes de dados publicamente disponíveis sobre a taxa da Hyperliquid - mas usando uma estimativa de dados até março de 2025, podemos prever um volume de recompra mensal de cerca de ~2.5M HYPE ou ~$35M impulsionado pelo AF usando 54% do volume de perps.

- A staking do HYPE foi lançada em 30 de dezembro de 2024, oferecendo um rendimento anual de cerca de 2,5% com base nas recompensas de PoS, modelado após o sistema da Ethereum.

- Atualmente, 30M tokens de propriedade do usuário (excluindo os 300M tokens da equipa/fundação) estão bloqueados.

O que vem a seguir?

A Hyperliquid poderia introduzir um modelo de partilha de taxas em que uma parte das taxas de transação on-chain vai diretamente para$HYPEdetentores, criando um ecossistema mais sustentável e recompensador — embora se possa argumentar que o modelo atual cria mais volatilidade tanto no lado positivo como no negativo.

O Hyperliquid ganha taxas de negociação e leilões HIP-1, com futuras fontes de receita como transações HyperEVM. Em vez de usar todas as taxas para recompras ou incentivos, uma parte poderia ser:

- Distribuído para $HYPEdetentores com base nas suas participações ou montantes apostados.

- Recompensando os stakers de longo prazo, incentivando uma participação mais profunda.

- Mantido num tesouro comunitário, permitindo que a governança decida o seu uso.

Possíveis Modelos de Distribuição:

- Partilha direta de taxas - uma parte das taxas de negociação é convertida em USDC (ou mantida como HYPE) e distribuída periodicamente, como dividendos.

- Recompensas impulsionadas pela aposta - apenas apostadas$HYPEganha uma parte, recompensando o compromisso a longo prazo.

- Modelo Híbrido — uma mistura de redistribuição de taxas e recompras HYPE para equilibrar o suporte de preços e incentivos.

Ethena

Ethena Labs é agora um dos 5 melhores protocolos DeFi em TVL, trazendo mais de $300M em receitas. Com este crescimento, a proposta de mudança de taxas da Wintermute foi aprovada pelo Comité de Risco da Ethena.

Neste momento, 824M ENA ($324M) estão bloqueados, representando 5,5% do fornecimento total, mas os bloqueadores só ganham recompensas em pontos e airdrops não reclamados de ENA - não recebem uma parte das receitas da Ethena.

Ativar o interruptor de taxas daria aos stakers exposição direta à receita e fortaleceria a governança da DAO ao alinhar incentivos com os detentores de ENA.

Ethena ganha dinheiro principalmente capturando as taxas de financiamento do mercado perp. Atualmente, 100% dos lucros vão para os stakers USDe e o fundo de reserva. Nos últimos três meses, a receita mensal tem sido em média de $50M.

O que precisa acontecer antes da mudança de taxa?

O Comité de Risco definiu cinco referências-chave para garantir que a Ethena esteja numa posição sólida antes de partilhar receitas.

Progresso atual sobre essas métricas:

- Objetivo de Fornecimento USDe: 6B ❌ - Apenas a 9% de distância do objetivo.

- Receita Cumulativa: $250M+ ✅ – Ultrapassou esta marca em janeiro, agora está em $330M.

- Integração da Exchange: Binance/OKX ❌ – Ainda sem cronograma, mas a Binance agora detém 4 milhões de USDe.

- Rácio do Fundo de Reserva ≥ 1% do Fornecimento USDe ✅ - Com $61M em reservas, Ethena pode suportar 6.1B USDe.

- sUSDe vs sUSDS APY Spread ≥ 5% ❌ – O spread apertou devido à queda do mercado, mas poderá expandir novamente.

O que se segue?

Ethena está perto de atingir suas metas, mas a mudança de taxa permanecerá em espera até que todos os benchmarks sejam atingidos. Enquanto isso, a equipe está focada em aumentar o fornecimento de USDe, garantir mais integrações de câmbio e monitorar as condições de mercado.

Uma vez que tudo estiver no lugar, os detentores de ENA podem começar a beneficiar da partilha de receitas.

Considerações Finais:

A mudança em direção à acumulação de valor para os detentores de tokens está a acelerar em todos os principais protocolos DeFi. Aave, Ethena, Hyperliquid e Jupiter estão todos a implementar programas de recompra, mudanças de taxas e novas estruturas de incentivos para tornar os seus tokens mais valiosos para além da especulação.

Esta tendência reflete um movimento mais amplo da indústria em direção à tokenomics sustentável, onde os projetos se concentram na distribuição de receitas reais em vez de incentivos inflacionários.

Aave está a alavancar as suas reservas profundas para apoiar recompras e melhorias de governação, Ethena está a trabalhar para permitir partilha direta de receitas para os stakers, Hyperliquid está a otimizar os seus modelos de recompra e distribuição de taxas, e Jupiter está a bloquear tokens recomprados para estabilizar o fornecimento.

À medida que as condições regulatórias se tornam mais favoráveis e o DeFi continua a amadurecer, os protocolos que alinham com sucesso os incentivos com as suas comunidades irão prosperar.

Aviso legal:

- Este artigo é reproduzido a partir de [Marco Manoppo]. Todos os direitos autorais pertencem ao autor original [Marco Manoppo]. Se houver objeções a esta reimpressão, entre em contato com o Gate Learnequipa e eles vão tratar disso prontamente.

- Aviso de responsabilidade: As opiniões expressas neste artigo são exclusivamente do autor e não constituem qualquer conselho de investimento.

- A equipe da Gate Learn faz traduções do artigo para outros idiomas. Copiar, distribuir ou plagiar os artigos traduzidos é proibido, a menos que mencionado.

Partilhar

Artigos relacionados

O que é o Gate Pay?

O que é o DyDX? Tudo o que precisa saber sobre a DYDX

O que é Uniswap?

Aptos: Um lar para DeFi's de Alto Desempenho

O que é Axie Infinito?